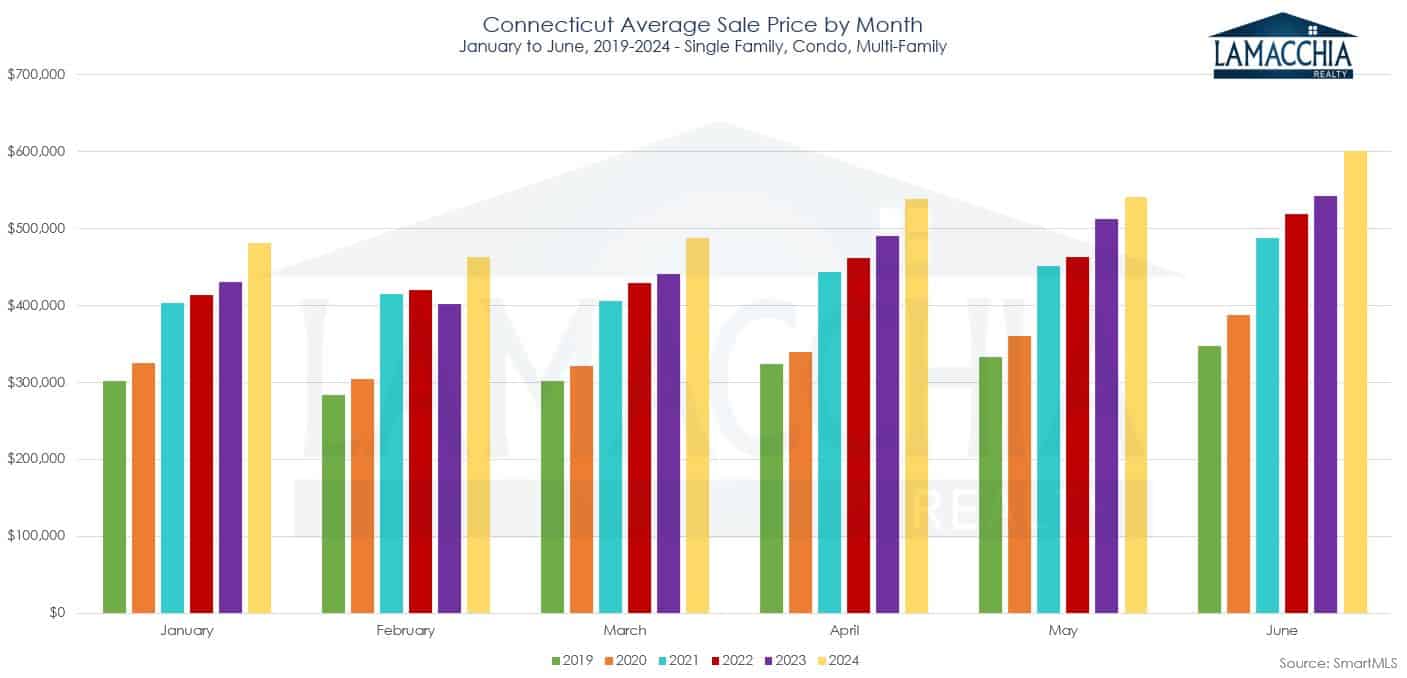

Average prices for homes climbed to $526,984 in the first half of 2024, a 9.9% increase from the first six months of 2023 at $479,322.

- Prices increased in all three categories: singles are up by 9.6%, condos are up by 9.8% and multis are up by 17.4%.

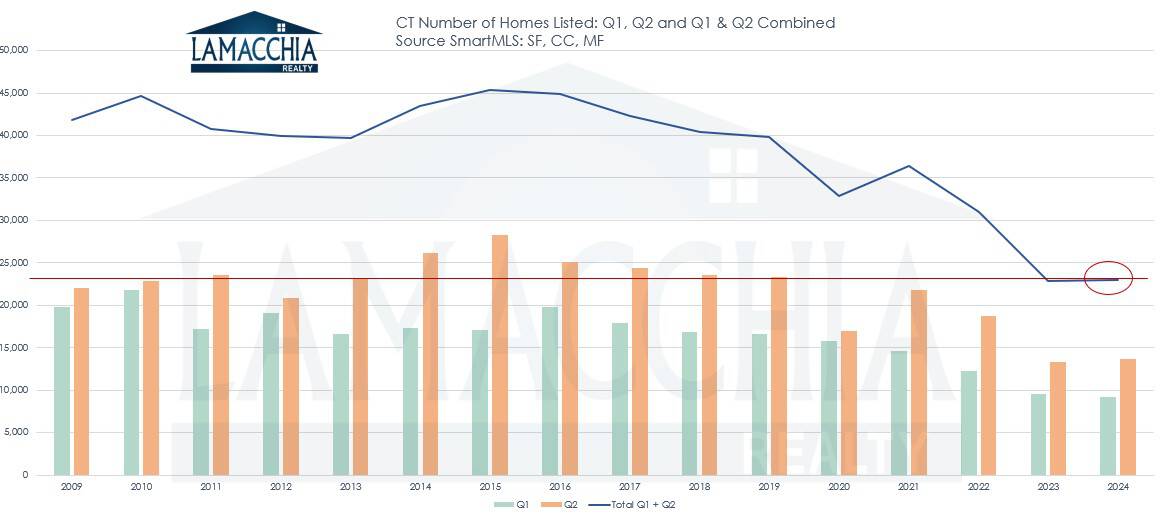

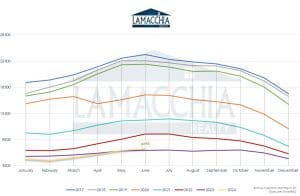

- Listings have slightly improved in volume so far this year by 1.9%, which contributes to the rise in inventory in CT. As of June 2024, inventory is finally reaching levels higher than last year (yellow line in the graph to the right) after starting the year with the lowest levels since 2017.

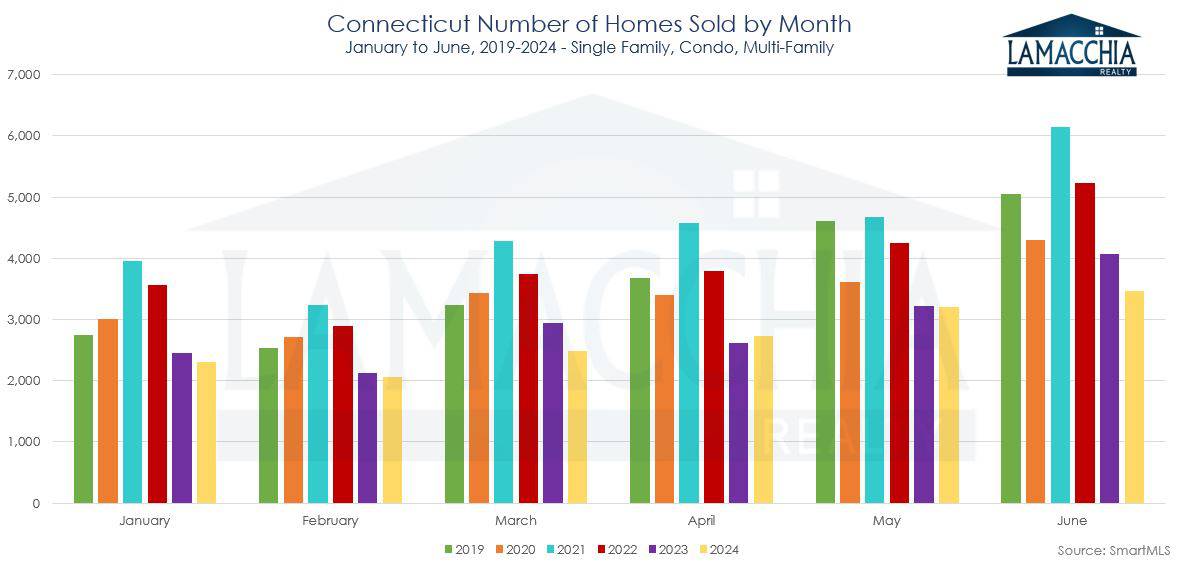

- Prices have been rising in Connecticut for years, but there was the Covid-era spike due to frenzied demand and since then a drop just hasn’t happened due to historically low inventory. Again, as mentioned earlier, the extremely tight Connecticut inventory will make it very unlikely that we will see a price drop.

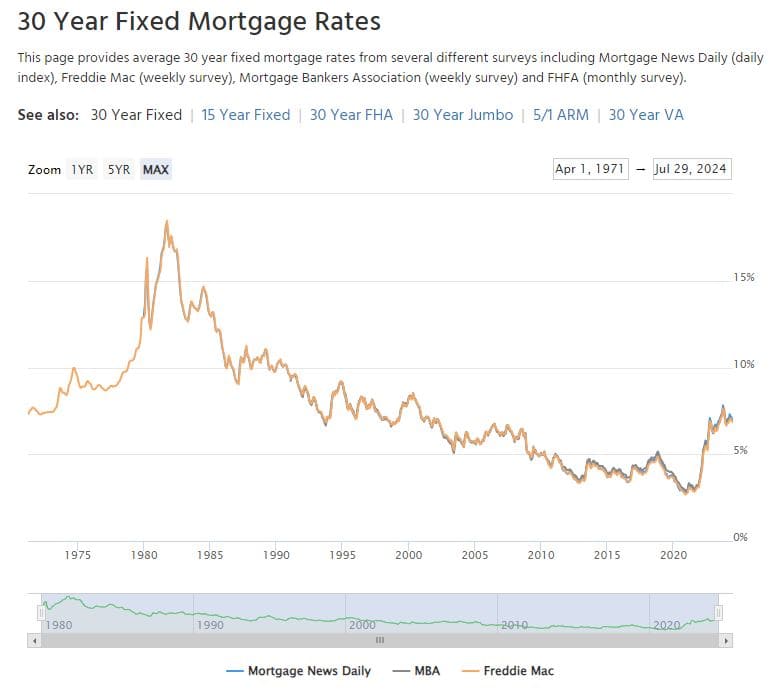

- If rates are a strong deterrent for buyers looking for more affordable monthly payments, there are several alternative options such as mortgage buydowns or assumptions that are worth exploring.

- The graph below shows how monthly prices over the past four years have steadily increased, with 2024 making wider strides than previous years.